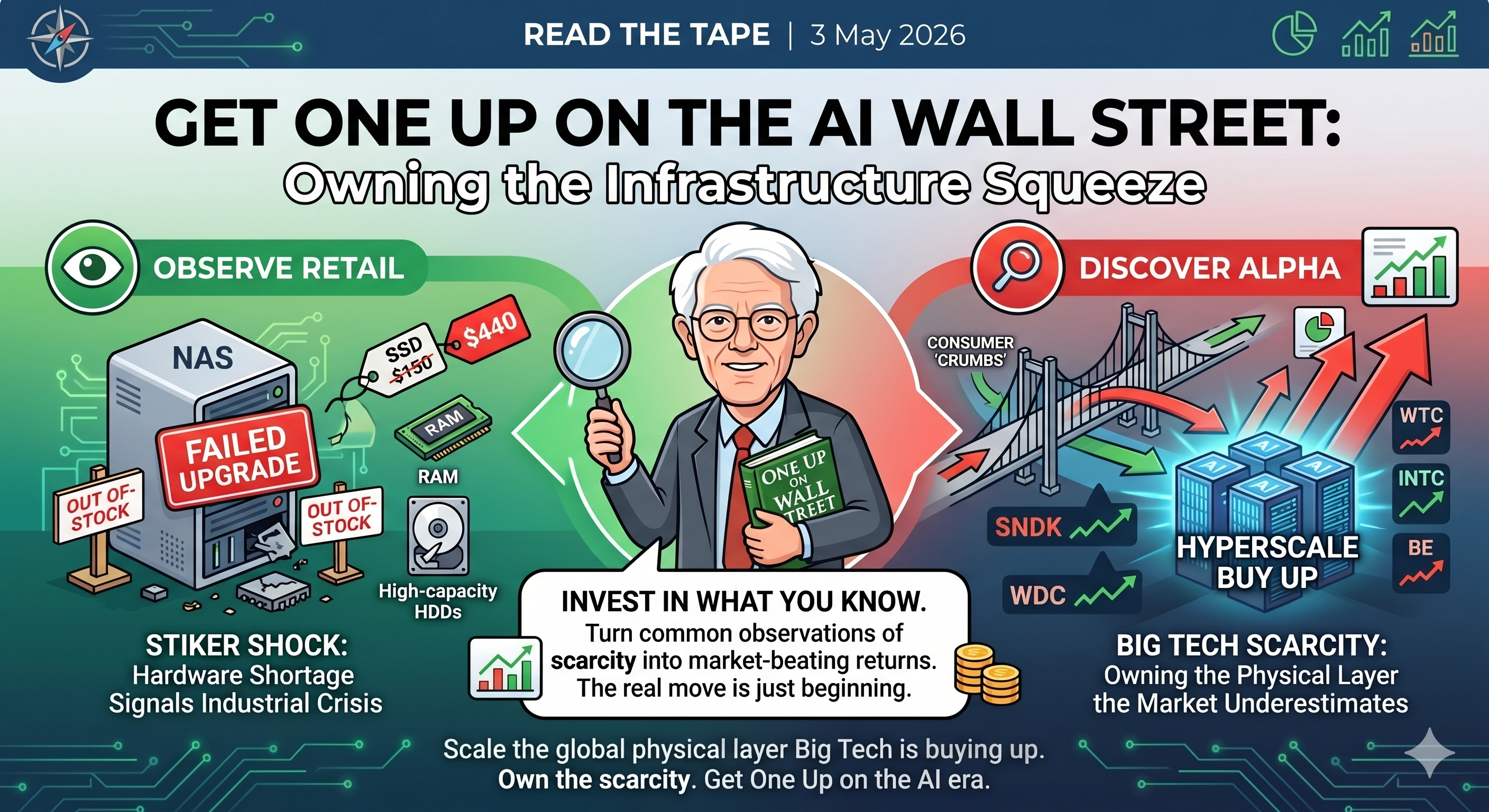

The Peter Lynch Reality Check

Legendary investor Peter Lynch famously preached “investing in what you know”. This week, the most reliable data didn’t come from a Bloomberg terminal – it came from a home server upgrade. If you’ve tried to source high-capacity storage lately like I have, you will notice a widespread shortage in consumer-grade hard disks and skyrocketing memory prices.

This isn’t just a personal inconvenience; it is a historic leading indicator of a supply chain in crisis, a sentiment echoed loudly by the r/DataHoarder Reddit community. As one user noted regarding the current state of the market:

“These HDD prices are getting crazy. An increase of 96.4% in 1 month for the same 26TB drive. $279.99 a month ago to $549.99 today”.

This “sticker shock” extends across the entire physical layer:

- SD Card: This enthusiast is now paying $45 for one Sandisk memory card while it can purchase two at $49 a few months ago. Same kind of panic in r/AskPhotography Reddit subgroup.

- SSDs: The price of the WD Black SN850X 2TB has surged nearly 3x, skyrocketing from roughly $150 at the end of 2025 to $440 in just six months. This SSD is frequently used in modern home and prosumer NAS devices to provide critical high-speed caching or primary storage tiers.

These personal server struggles are more than just anecdotal evidence of consumer pain; they are the loudest signal in the market today

The message is clear: hardware producers have decisively pivoted to satisfy hyperscaler demand, effectively starving the consumer market to feed the infrastructure wall.

Lead Story: The Storage Pivot (SNDK & WDC)

This week, the spotlight fell on the recently separated storage leaders, SanDisk (SNDK) and Western Digital (WD). Both companies delivered strong quarterly results that beat institutional estimates, yet both saw immediate sell-offs and recovered strongly the day after. For the observant investor, this “sell-the-news” price action is a gift.

While short-term funds are trimming after a historic run, the results reaffirmed powerful fundamental drivers:

- SanDisk (SNDK): Management is aggressively prioritizing shipments to support BiCS 8 QLC demand for the 4Q 26 Stargate ramp. Their shift toward multi-year engagements with firm financial commitments suggests earnings momentum is accelerating. Revenue guidance for next quarter 2Q 26 is 5% above analyst’s forecasts.

- Western Digital (WD): Even as a pure-play HDD business, WD is seeing a resurgence as “cold storage” requirements for massive AI datasets explode.

Cracking the Infrastructure Wall

The theme we have been tracking, the new AI reality, is now playing out across the entire physical stack. We aren’t just looking at chips; we are looking at the Industrialization of AI. The recent quarterly results by the tech companies are all telling different sides of the same story. It confirms the physical layer is the new scarcity.

- Intel (INTC): Finally clearing its dot-com bubble high of $75.83 was the ultimate validation. Intel’s Q1 print proved it is bridging the gap to a “foundry reality” that Western infrastructure requires.

- Energy Infrastructure (BE & GEV): The power bottleneck is real. Bloom Energy (BE) recently cemented its role with the Oracle Project Jupiter deal (2.45 GW of on-site power), while GE Vernova (GEV) reported a record quarter with $5B in free cash flow.

- Cooling & Connectivity: Vertiv (VRT) continues to defy gravity with a $15B backlog, driven by the desperate need for liquid cooling as rack densities skyrocket.

Ignoring the Noise, Owning the Scarcity

While the indices may take a breather, the AI infrastructure wall are providing immense opportunity; we haven’t even reached the middle innings yet. The volatility in storage this week isn’t a signal of a top; it’s a re-fueling stop for the next leg up.

The major indices, Nasdaq, S&P and PHLX Semiconductor Sector Index, are maintaining close to record high levels. While geopolitical “war talk” persists without solid progress, the market has decisively looked past those headlines to focus on the massive, physical buildout required to sustain the AI era.

The information provided in this note is for educational and informational purposes only and does not constitute financial, investment, or professional advice.

Leave a Reply